Your Scouting Legacy

To establish your Scouting legacy you can make a charitable bequest in your will, make a gift of an IRA or a life insurance policy. Estate planning with these vehicles reduces the tax liability for your heirs. In addition, your final gift to Scouting also cements your Scouting legacy within your family ensuring your descendants know the important role Scouting should still continue to play in their lives.

Curious how changes to the IRS tax code impacts your estate planning? This guide can help.

A bequest is one of the easiest gifts to make. With the help of an advisor, you simply include language in your will or trust specifying a gift to be made to Boy Scouts of America as part of your estate plan. You can establish your legacy, and it remains revocable at any time during your life. For donors with taxable estates, charitable bequests are completely tax deductible when distributed. There are many types of bequests you can consider, including:

- General—A designated amount of money, such as “$10,000.”

- Specific—A certain item, such as “my 100 shares of IBM stock,” “my home at 123 Main Street,” “my original Norman Rockwell painting,” etc.

- Percentage—A designated percentage of your estate, such as “10 percent.” This helps protect against inflation, reducing the value of your bequest.

- Residuary—Gives Scouting all or a percentage of anything left after all general and specific bequests are satisfied.

- Contingent Bequest—Only takes effect if another bequest fails, such as “If my father should predecease me, then this should go to the XYZ Council, BSA.”

Many donors establish “testamentary” charitable trusts in their wills. These are just like the “regular” annuity trusts or unitrusts—the only difference is they are funded or created in your will. Also, for donors who use living trusts, Scouting and other charities can easily be included in those.

Recent tax law changes kept the existing marital deduction, allowing an unlimited transfer amount between spouses. But it greatly increased the lifetime estate and gift exclusion, allowing the transfer of up to almost $11,700,000, at any time during life or at death, to anyone, tax free, regardless of marital status. For example, a married couple may transfer unlimited amounts between them, and another $23.4 million at any time to anyone else they want (e.g. children, grandchildren, etc). For over 99% of taxpayers, this eliminates estate tax concerns, greatly increases the amounts available to pass to family and charities, and reduces the need to create trusts just to avoid transfer taxes. The recent tax law changes also increased the annual exclusion to $15,000 per year/per person- additional amounts that can be transferred to anyone without transfer tax and without impacting your lifetime exclusion.

If you already have a will and want to make some simple changes, you can do so with a codicil. A codicil is a simple addition or amendment to an existing will. As with wills, codicils involve certain signing formalities and can be revoked or changed during your lifetime. But no matter what your charitable plans, make sure you have a valid will and regularly review it so it meets the changing needs of you and your family.

Retirement fund assets can be one of the most significant assets left in an estate. Unfortunately, the gift of an IRA to a child or grandchild—or anyone other than a spouse or charity—can be one of the costliest gifts of all. Retirement funds given to children or grandchildren can be double taxed, or worse, leaving only a fraction for your intended beneficiaries.

ESTATE PLANNING TIP

Name Scouting and other charities as a survivor beneficiary | Many donors find gifts of IRA assets to charity to be an effective, taxwise way to give. Naming your local council as an alternate or contingent beneficiary of your retirement accounts is as simple as requesting a change-of-beneficiary form from your plan administrator. IRAs and other retirement accounts may also be used to fund a testamentary charitable trust.

Are you age 70 1/2 or older this year? If so, there are special IRA gift opportunities for you.

Tax free distributions to Scouting and other charities from your IRA are now available!

- Donors age 70 ½ or older at the time of the distribution, may make distributions of up to $100,000 a year directly to charities and avoid paying any tax on the distributions. There is no tax deduction, but the distribution counts toward your annual minimum required distribution, and it is not taxed to you when distributed.

Younger donors who do not qualify for the tax free IRA distributions may still make contributions from their IRA. They will be taxed on the withdrawal, but are entitled to a charitable tax deduction that may offset tax paid for the distribution. But please talk to your advisors – this may affect your tax bracket, and may not work unless you itemize your deductions.

Do you have insurance policies no longer needed for their original purpose? Do you have a policy:

- providing money for a spouse or children, who no longer need it?

- covering a mortgage on a home or other property that’s now paid off?

- covering educational expenses that no longer exist?

- protecting a business you no longer own or that has other coverage at this point?

ESTATE PLANNING TIP

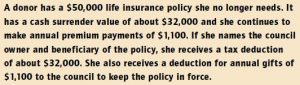

Donate a new or existing policy to Scouting and your tax deduction is about equal to the policy’s cash surrender value. | It may be beneficial to donate such policies and take the tax deduction. In general, you can also deduct any annual amounts paid to keep the policy in effect.

Example of a Life Insurance Gift