Gifts Can Generate Income?

It pays to support The Boy Scouts of America National Foundation. Literally. With the income-producing gift options below, you can create a secondary source of revenue or augment your retirement assets while enjoying major tax incentives.

A charitable gift annuity is a simple contract between a donor and the BSA. In exchange for a gift, the BSA agrees to make payments to the donor or others chosen by the donor. These payments are made for life, to one or two individuals, and guaranteed by the general assets of the Boy Scouts of America. The donor also receives an income tax charitable deduction.

The gift may be of cash, stocks, bonds, or shares in a mutual fund. The minimum gift required to receive a charitable gift annuity from the BSA is $10,000. You cannot add to a charitable gift annuity once it is made, but you may set up as many as you wish. The donor may choose anyone to receive quarterly payments for life, though all beneficiaries must be at least 60 years of age at the time of the contract. Most donors select themselves and/or a spouse to receive the payments. The annual payout amount depends on the age of the beneficiaries. The older the beneficiary, the larger his or her payment. As of 2016, the gift annuity rates range from 4.4 percent to 9 percent for beneficiaries between the ages 60 and 90. Part of each payment is taxable income, but part of each payment is often tax-free as a partial return of principal. This may increase the effective rate of return, depending on your tax bracket and the cost basis of your gift.

At the end of the gift annuity term (the lifetime of the payment recipient(s)), the remaining value of the original gift is removed from the gift annuity fund and given to the council chosen by the donor. Charitable gift annuities are handled through the Charitable Gift Annuity Program at the BSA National Service Center; this relieves local councils from administrative burdens, state filings, and fees.

After making your gift to The Boy Scouts of America National Foundation, you receive a fixed annual dollar amount for life, along with an income tax deduction. The principal remaining at your death then passes on to The Boy Scouts of America National Foundation.

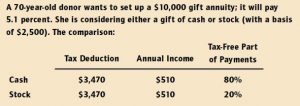

Example of a Gift Annuity

Deferred Gift Annuities

Some donors set up a gift annuity —to get the income tax deduction now—but defer the start of the payments until a later time. Payments may be deferred for as long as the donor wants. The annuity is often larger for deferred gift annuities. This strategy may be useful for donors currently in a high income bracket and planning for retirement. Unlike IRAs and other retirement alternatives with contribution limits, there is no limit as to how much you can place in a deferred gift annuity.

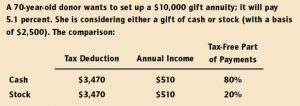

Example of a Deferred Gift Annuity

We regularly establish remainder trusts and lead trusts for donors and their families. These trusts can make regular income distributions to the donor, family, or BSA, and are very flexible in their terms. When the trust ends, the funds may go to Scouting or to the donor and family, depending on the donor’s wishes.

Charitable Remainder Trusts

One of the most flexible ways for you to make a major gift to Scouting is to use a charitable remainder trust, CRT. Your gift is placed in a CRT and it sells and reinvests the assets. The trust makes regular payments to you and/or others for a specific number of years or for one or two lifetimes. CRTs may be funded with cash, stocks, bonds, land, and even other assets. The payout rate can be chosen by the donor. Payments are based on the fair market value of the gift placed into the trust. Payments can be a specific amount (annuity trust) or a fixed percentage (unitrust).

Trusts with percentage payouts are revalued each year—as the principal grows in value, the annual payment also grows. When the trust ends, the principal goes to the BSA, as directed by the donor. Often a local bank or trust company is chosen as trustee. The donor or other family members may serve as trustee, but that person should be experienced with financial planning instruments and tax filings.

The BSA Foundation may serve as trustee for trusts funded with $100,000 or more in cash, stocks, or other securities (if funded with real estate, the property value must be $250,000 or more). The timing and rates of payment, investment philosophy, type of income, and other details can be tailored to provide a financial planning tool that is creative, fiscally sound, and responsive to your needs. You are entitled to an income tax deduction when you create your trust, and you may avoid capital gains tax and increase your cash flow by funding the trust with low-yielding, highly appreciated assets.

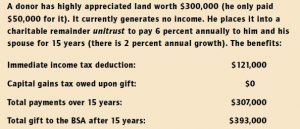

Example of a Charitable Remainder Trust

Charitable Lead Trusts

This option helps you avoid the heavy gift and estate tax burdens incurred by directly transferring property to family members. Unlike the other trust options, a lead trust pays income to The Boy Scouts of America National Foundation from the start for a specified term of years, and the principal eventually reverts back to you or other non-charitable beneficiaries. Under certain conditions, the lead trust will generate an immediate income tax deduction.

Some think of a lead trust as a partnership between themselves and a charity. Some see it as a “mirror image” of a charitable remainder trust. To others, it is a loan to charity. But most people agree that the lead trust is a great way to make a significant gift to Scouting using funds that eventually will return to you or your loved ones. It’s also a great way to pass assets to your loved ones at very little cost.

Your assets are placed in a lead trust for a period you choose—either a number of years or measured by someone’s lifetime. During this period, the income is paid to the council of your choice (and you determine how much that will be). Trust earnings not needed for income are accumulated in the trust principal. At the end of the trust, the principal (and any growth) is distributed either to the donor or to anyone selected by the donor—tax free. Tax deductions are largely determined by three factors: who eventually receives the principal, the term of the trust, and the annual payout. In general, if the trust returns to the donor, an income tax deduction is available. If the trust goes to someone other than the donor, only a gift tax deduction is available.

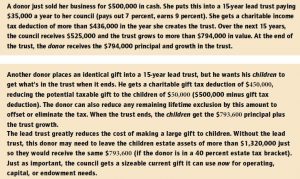

Example of a Charitable Lead Trust